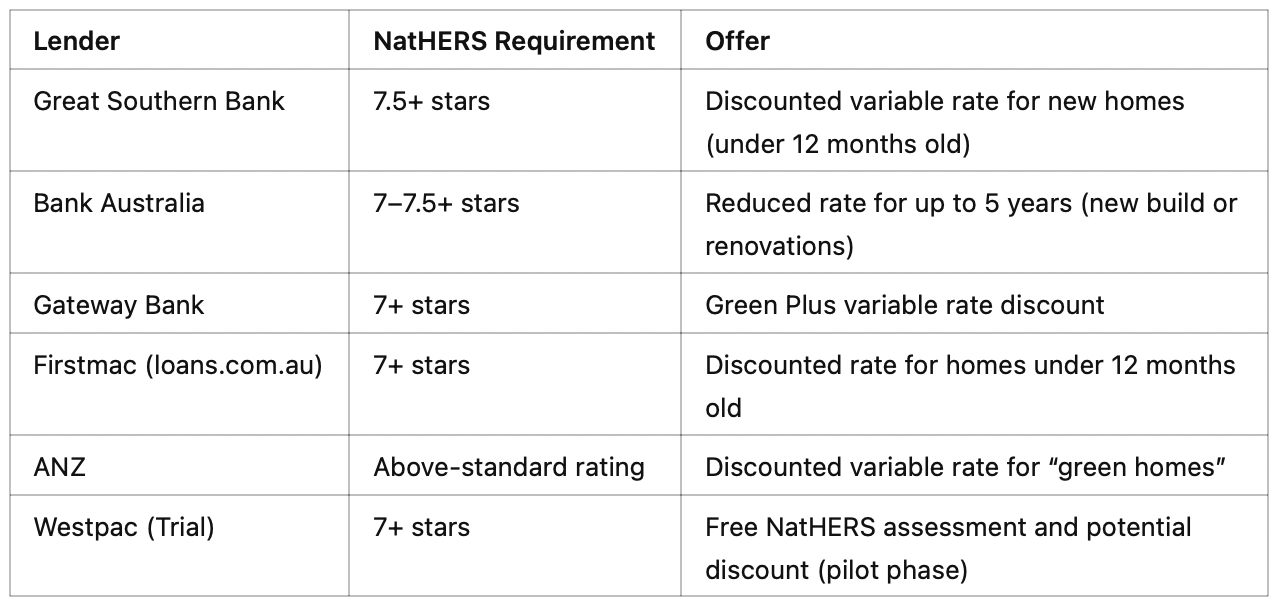

Features of Green Home Loans

• Discounts of 0.05% to 0.25% below standard rates

• Typically apply to variable rate loans, though some lenders offer fixed or introductory green rates

• Can be combined with features like offset accounts, redraw, and flexible repayment options

• Some loans also apply to renovations or retrofits, not just new builds

How to Qualify for a Green Home Loan

1.

Build or buy a NatHERS-rated home (7.0+ stars)

Start with energy-efficient design and materials, working with a builder who understands sustainability and NatHERS compliance.

2.

Obtain a NatHERS certificate

This must come from an accredited assessor and be included in your loan application.

3.

Apply with a lender offering green loan options

Submit your plans or certificate to secure the discount. For new builds, discounts are typically confirmed once construction is complete and the rating is verified.

At PB Property we recommend using a

Mortgage Broker as they will be able to assist you with the best product and a more personalised approach.

We have a panel of qualified independent

Mortgage Brokers that we can refer you to and make this process smooth.

Why Are Banks Offering These Discounts?

Aside from environmental responsibility, lenders have real financial motivations for offering green loan incentives:

• High-rated homes cost less to run, lowering default risk

• Higher resale value enhances loan security

• Aligns with ESG commitments and government net-zero targets

The Bottom Line: Sustainability Pays

Green home loans are not just a trend—they’re a smart financial move for investors and homeowners looking to future-proof their properties and reduce costs. With banks now actively supporting sustainable housing, the opportunity to benefit from energy-efficient design has never been greater.

How PB Property Can Help You Invest Smarter

At PB Property, we go beyond just sourcing land—we work hand-in-hand with investors to ensure their house and land packages are designed for both sustainability and financial performance.

Here’s how we can support your green investment journey:

• Connect you with expert builders who understand the NatHERS rating system and can deliver homes with 7.0–7.5+ stars

• Guide your design process to ensure compliance with lender requirements for green loans

• Maximise your financing options by helping you qualify for interest rate discounts through energy-efficient building choices

• Future-proof your investment by building homes that appeal to eco-conscious buyers and tenants, all while saving you money

Ready to Build Smarter?

Let us help you create a home that’s efficient, bank-friendly, and investment-ready.

Contact PB Property today and

ask how we can help you build a NatHERS-rated home that qualifies for a green loan and sets your portfolio up for long-term growth.