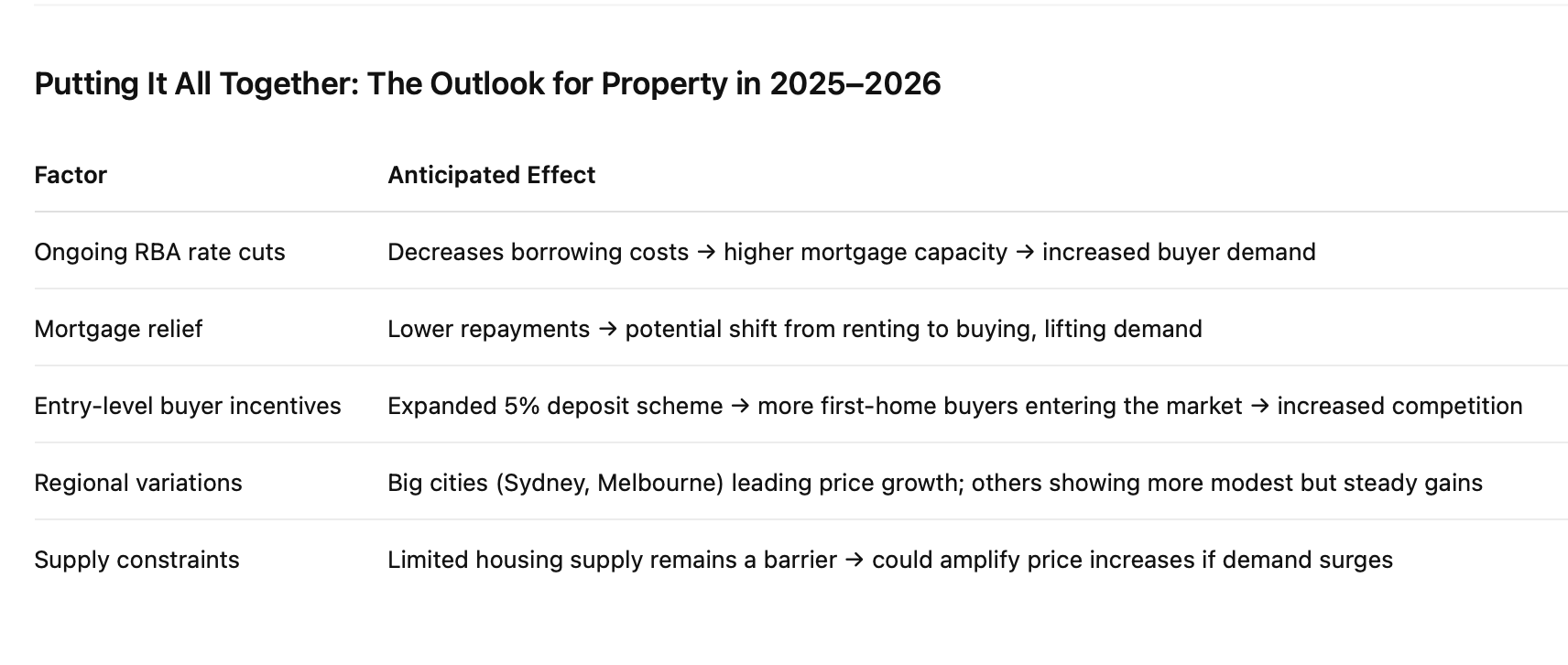

As if cheaper borrowing wasn’t enough to heat things up, January 2026 is set to bring another wave of market-changing policies. The government will expand the

5% Deposit Guarantee Scheme to all first-home buyers, regardless of income, and raise the property price caps. Buyers using the scheme won’t need to pay

Lenders Mortgage Insurance (LMI), which can save tens of thousands of dollars. This is a massive boost for first-home buyers, and it’s likely to draw even more competition into an already tightening market.

There’s also a

two-year ban on foreign buyers purchasing established property, which remains in place until at least 2027. While this may reduce some competition at the high end, the effect at the entry level could be the opposite — more local buyers fighting for the same limited stock. With supply still struggling to keep up with demand, the combination of rate cuts and policy changes could create a perfect storm for price growth.

So, what does this mean for you? If you’re a homebuyer, you may find that while the cost of borrowing falls, the race to secure a property gets tougher. The months ahead could see open homes buzzing with more buyers, auctions heating up, and prices edging higher. For sellers and investors, however, the landscape is looking promising. The mix of cheaper finance, expanded buyer incentives, and persistent supply constraints is setting the stage for potentially significant gains in property values.

Whether you’re buying, selling, or just watching from the sidelines, one thing is clear — the next 18 months in Australian real estate are going to be anything but dull.

This is why you need someone in your corner to help you navigate the crazy times ahead.

Book a complementary call and lets have a chat and see how we can assist you.