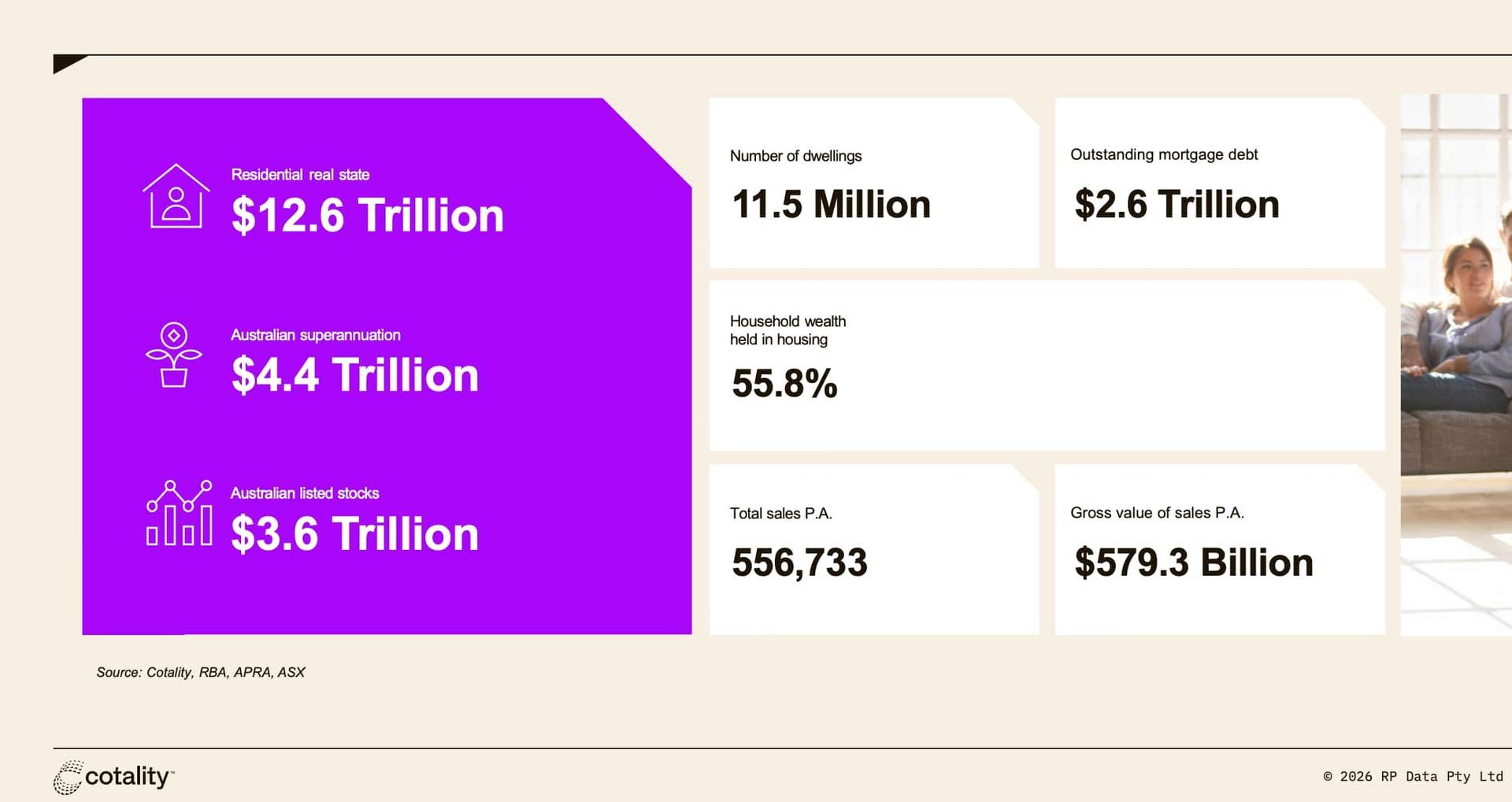

Australia's housing market remains remarkably resilient in 2026, continuing to deliver capital growth despite affordability challenges, elevated interest rates and softer buyer demand. While national dwelling values are still rising, the pace of growth has clearly moderated compared to the strong gains recorded throughout 2025.

According to the latest Cotality (formerly CoreLogic) Monthly Housing Chart Pack, national dwelling values increased by 8.8% over the 12 months to May 2026, although quarterly growth slowed to just 0.6%. This suggests the market is transitioning from a period of rapid expansion into a more balanced phase, where local market fundamentals will play a greater role in determining performance.

The data reveals a market of two halves. Perth, Brisbane, Adelaide and Darwin continue to produce exceptional growth, while Sydney and Melbourne are beginning to show signs of weakness. Investors and homebuyers alike will need to be increasingly selective as market conditions evolve.

The Positives: Why Property Continues to Perform

Strong Annual Growth Across Most Markets

Although national growth has moderated, an annual increase of 8.8% remains a strong result by historical standards.

Perth continues to lead the nation with dwelling values increasing 25.8% over the year, followed by Darwin at 20.3% and Brisbane at 19.1%. Adelaide also delivered impressive growth of 12.3%, demonstrating that affordability-driven markets continue to attract both owner-occupiers and investors.

What is particularly notable is that these markets are not only growing but have reached new record highs. Brisbane, Adelaide, Perth and Darwin are all sitting at peak values, highlighting the ongoing imbalance between housing supply and demand.

Units Are Becoming the New Growth Story

One of the most interesting trends emerging in 2026 is the outperformance of units compared to houses.

Unit values are now rising faster than detached housing across Sydney, Brisbane, Adelaide and Perth. Brisbane units recorded annual growth of 21.8%, outperforming houses at 18.6%, while Perth units surged 27.8% compared with 25.6% growth for houses.

This trend reflects growing affordability pressures. As detached homes become increasingly expensive, buyers are shifting towards higher-density housing options that offer a more affordable entry point into desirable locations.

For investors, this may signal renewed opportunities in well-located apartments and townhouses, particularly in markets experiencing strong population growth.

Rental Markets Remain Extremely Tight

Investors continue to benefit from one of the strongest rental markets in decades.

The national vacancy rate sits at just 1.5%, significantly below the long-term average of 2.5%. Rental values increased 5.9% nationally over the year to May, with growth occurring across both capital city and regional markets.

Several markets recorded particularly strong rental increases:

- Perth: 7.5%

- Hobart: 8.0%

- Regional Tasmania: 10.3%

- Regional Western Australia: 8.7%

The combination of strong rental growth and slowing price growth has also improved rental yields. National gross rental yields have risen to 3.62%, while regional markets now offer average yields of 4.2%.

For investors focused on cash flow, this represents a significant improvement compared to the low-yield environment that characterised much of the previous decade.

Investor Activity Continues to Rise

Despite higher borrowing costs, investor participation remains strong.

Investors now account for 40.3% of all new lending nationally, the highest proportion since 2016. Investor lending growth continues to outpace owner-occupier borrowing in most states, suggesting many investors still see value in residential property despite the challenging economic backdrop.

This level of investor confidence is particularly encouraging given the higher interest rate environment, indicating long-term belief in the strength of Australia's housing market.

The Negatives: Warning Signs Emerging Beneath the Surface

Growth Momentum Is Clearly Slowing

While annual growth remains positive, the market is losing momentum.

National dwelling values rose only 0.6% over the three months to May, down significantly from the stronger growth rates seen throughout 2025. Cotality notes that annual growth peaked at 10.0% in February and has since eased to 8.8%.

This slowdown is evident across most markets, including Perth and Brisbane, where growth remains positive but is no longer accelerating.

Housing markets typically move in cycles, and current conditions suggest Australia may be entering a period of slower capital growth rather than another phase of rapid appreciation.

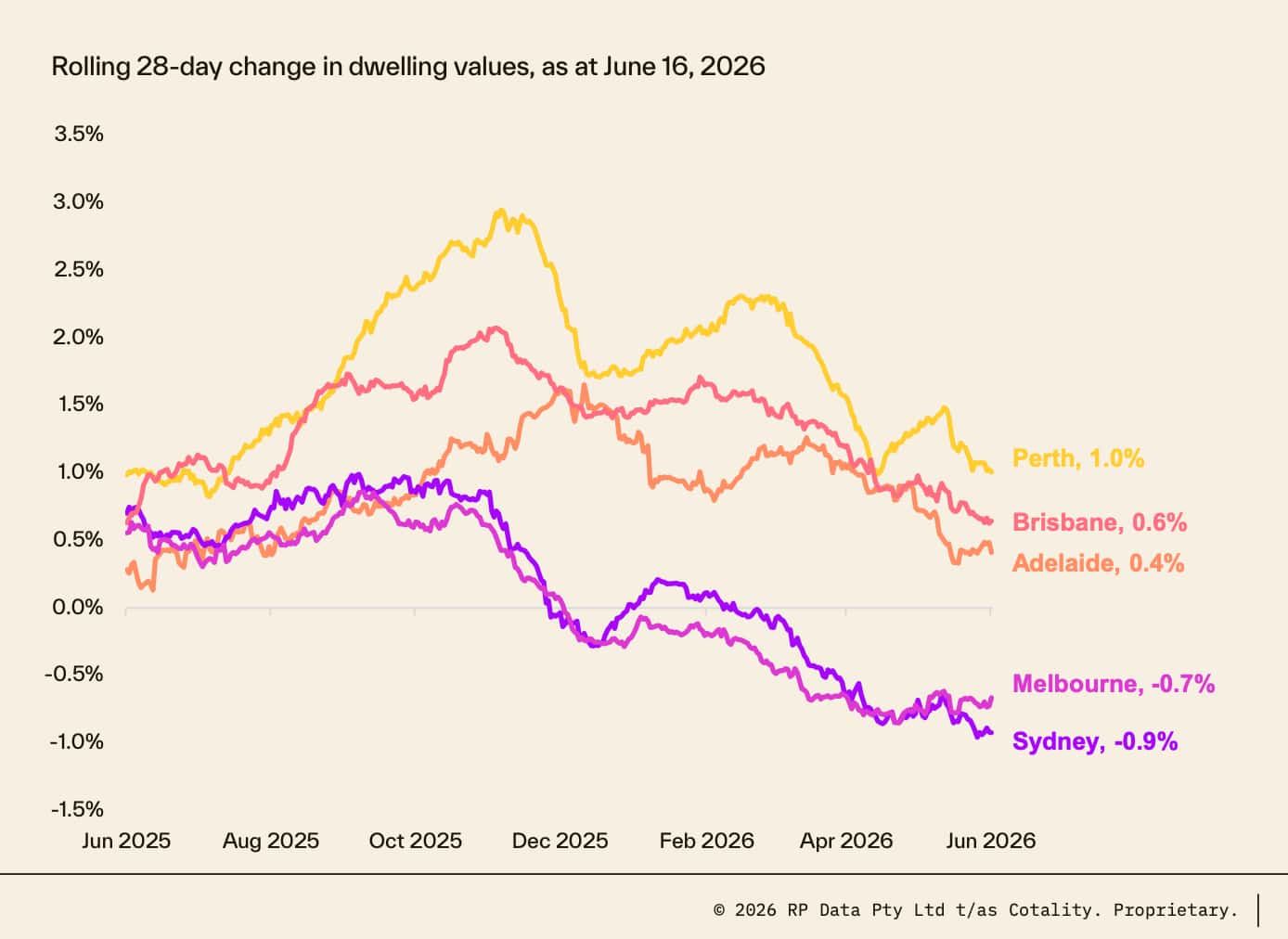

Sydney and Melbourne Are Moving Backwards

Australia's two largest housing markets are showing signs of weakness.

Sydney dwelling values fell 2.1% over the quarter and are now 2.1% below their November 2025 peak. Melbourne values declined 2.3% over the quarter and remain 3.2% below the record high reached back in March 2022.

On a rolling 28-day basis, both cities are currently recording negative growth rates, highlighting deteriorating market conditions.

Given that Sydney and Melbourne account for a substantial share of Australia's housing market activity, continued weakness in these cities could place additional downward pressure on national growth figures over the coming months.

Buyers Are Becoming More Cautious

Several indicators suggest buyer demand is weakening.

Homes are taking longer to sell, with median days on market beginning to rise during 2026. Nationally, properties now take a median of 28 days to sell, while some regional markets are experiencing much longer selling periods.

Vendor discounting is also increasing. Sellers across the combined capital cities are now accepting discounts of around 3.3% from their original asking prices, indicating buyers have gained greater negotiating power.

Auction markets tell a similar story. Clearance rates have fallen from cyclical highs of around 72% in late 2025 to below 60% during 2026, reflecting softer demand and improving supply levels.

Interest Rates Remain a Major Challenge

Perhaps the biggest headwind facing the market remains borrowing costs.

The Reserve Bank has kept the cash rate at 4.35%, while average variable mortgage rates have climbed to approximately 5.9% for owner-occupiers and more than 6.0% for investors.

Cotality suggests that any meaningful rate cuts are unlikely before 2027, meaning affordability pressures could persist for an extended period.

Higher mortgage repayments continue to reduce borrowing capacity, making it more difficult for many Australians to enter the market or upgrade to larger homes.

Affordability Is Becoming a Serious Concern

Housing affordability has deteriorated significantly across most capital cities.

Sydney remains Australia's least affordable market, with buyers needing a household income exceeding $178,000 to purchase a median-priced house. Brisbane is increasingly challenging affordability rankings as rapid price growth pushes required household incomes above $139,000 for a median house purchase.

Even entry-level housing is becoming more difficult to access. In Brisbane, buyers now require an annual household income of more than $86,000 to purchase a lower-quartile unit, an increase of almost $12,000 since January.

This growing affordability challenge could place a natural ceiling on future price growth as fewer households are able to meet lending requirements.

Outlook for the Remainder of 2026

Australia's housing market remains fundamentally supported by population growth, low vacancy rates, tight housing supply and strong labour market conditions. However, the extraordinary growth rates seen over the past two years are clearly fading.

Investors should continue to find opportunities in markets where affordability, population growth and rental demand remain favourable, particularly across Perth, Brisbane, Adelaide and selected regional areas. However, buyers should also be prepared for slower capital growth, increased negotiation opportunities and greater market variation between cities.

The second half of 2026 is likely to be defined by moderation rather than acceleration. Property values are still rising nationally, but the era of broad-based double-digit growth appears to be drawing to a close. For investors, success will increasingly depend on selecting the right market rather than simply relying on overall market momentum.

This is a great time to buy if you have the right professional next to you.

share to