While yields are often lower these areas deliver consistent long-term capital growth, superior infrastructure, and strong liquidity when it comes time to sell.

Green loans are specially designed home loan products that reward energy-efficient building choices. Offered by many Australian lenders, they provide lower interest rates

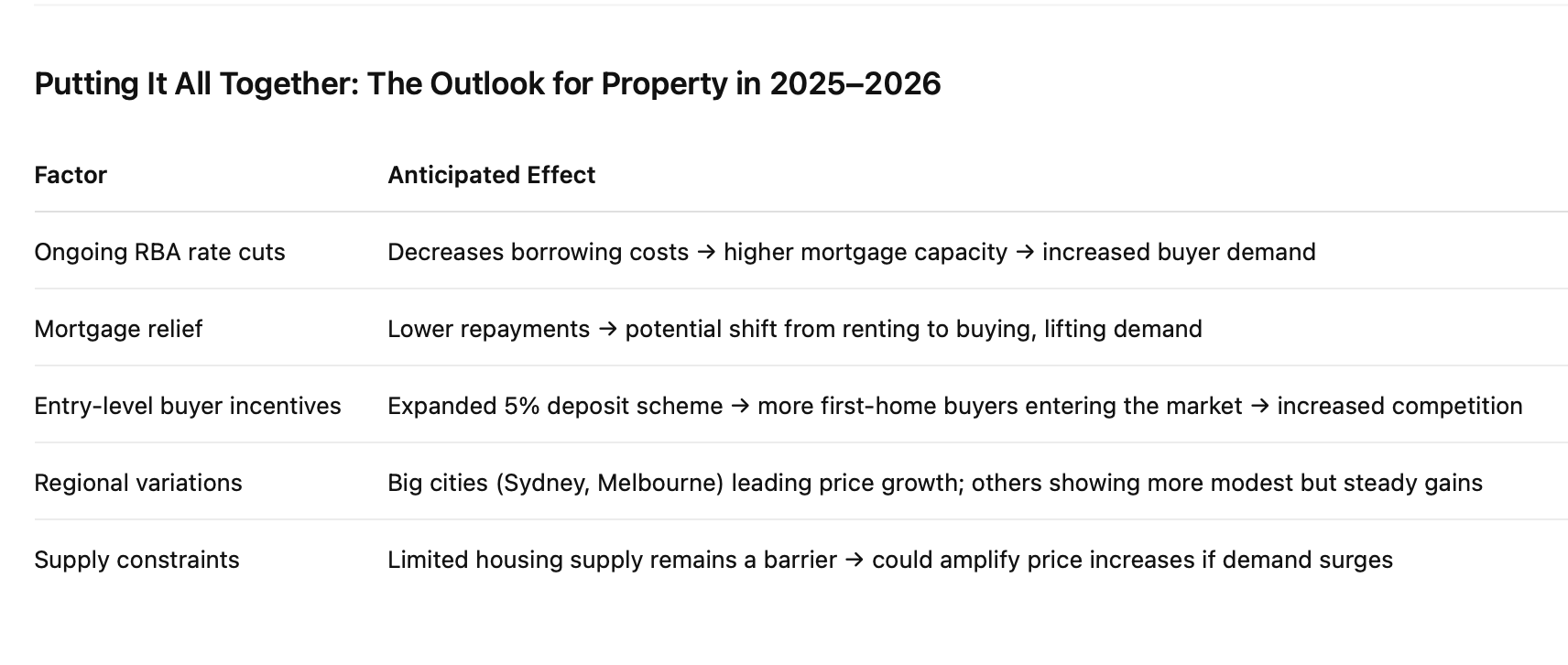

While the headlines might suggest doom and gloom, Melbourne is far from down and out. In fact, this moment of weakness may well be the turning point — the stage in the cycle where the city’s long-term fundamentals quietly gather momentum again. If you’ve been waiting for the right time to buy in Melbourne, 2025 could be your moment. Key Reasons Melbourne Is Still Attractive for Property Investors Market Recovery Signs: After a period of decline in 2024, Melbourne has posted several consecutive months of home price growth in 2025. This signals a market turnaround, with prices still below their previous peaks, offering a countercyclical opportunity for investors. Strong Population Growth: Melbourne continues to experience robust population growth, driving long-term housing demand. Migration has ramped up, supporting both the rental and sales markets. Undersupply of New Homes: Building approvals are at record lows, and there is a shortage of new dwellings. This supply constraint, combined with rising demand, is expected to place upward pressure on prices over the coming years. Infrastructure Investment: Ongoing investment in transport, schools, and amenities across Melbourne’s growth corridors is enhancing liveability and supporting property values. Affordability Relative to Other Capitals: Melbourne’s median home price is now lower than Sydney and some other capitals, making it more accessible for investors and first-home buyers. Interest Rate Cuts: Recent interest rate reductions in 2025 have improved buyer sentiment and affordability, helping to fuel renewed activity in the property market. Long-Term Growth Fundamentals: Melbourne’s diversified economy, strong employment hubs, and lifestyle appeal underpin its reputation as a resilient, long-term investment destination. Where Are the Opportunities? For those looking to enter the market now, focus on areas where fundamentals still stack up — even in a down market.